The Death of the Traditional 60/40 Portfolio

The Death of the Traditional 60/40 Portfolio

What has worked for decades may have rough sledding ahead

The traditional stock (60%) and bond (40%) allocation scheme in many financial planning circles has worked well for decades, going back to 1981 Reaganomics and 15% interest rates. Stocks were generally strong with a few rests along the way and with a long run down in interest rates, bond had a four decade bull market. Interest rates in recent years have gotten so low that they were banging up against 0%. Hard to imagine a world where they could go much lower.

That leaves a couple of possibilities: rates stay the same or they rise. Rising interest rates bring with them lower bond prices. In the 60/40 portfolio, that means that the conservative 40% of the portfolio will be swimming upstream.

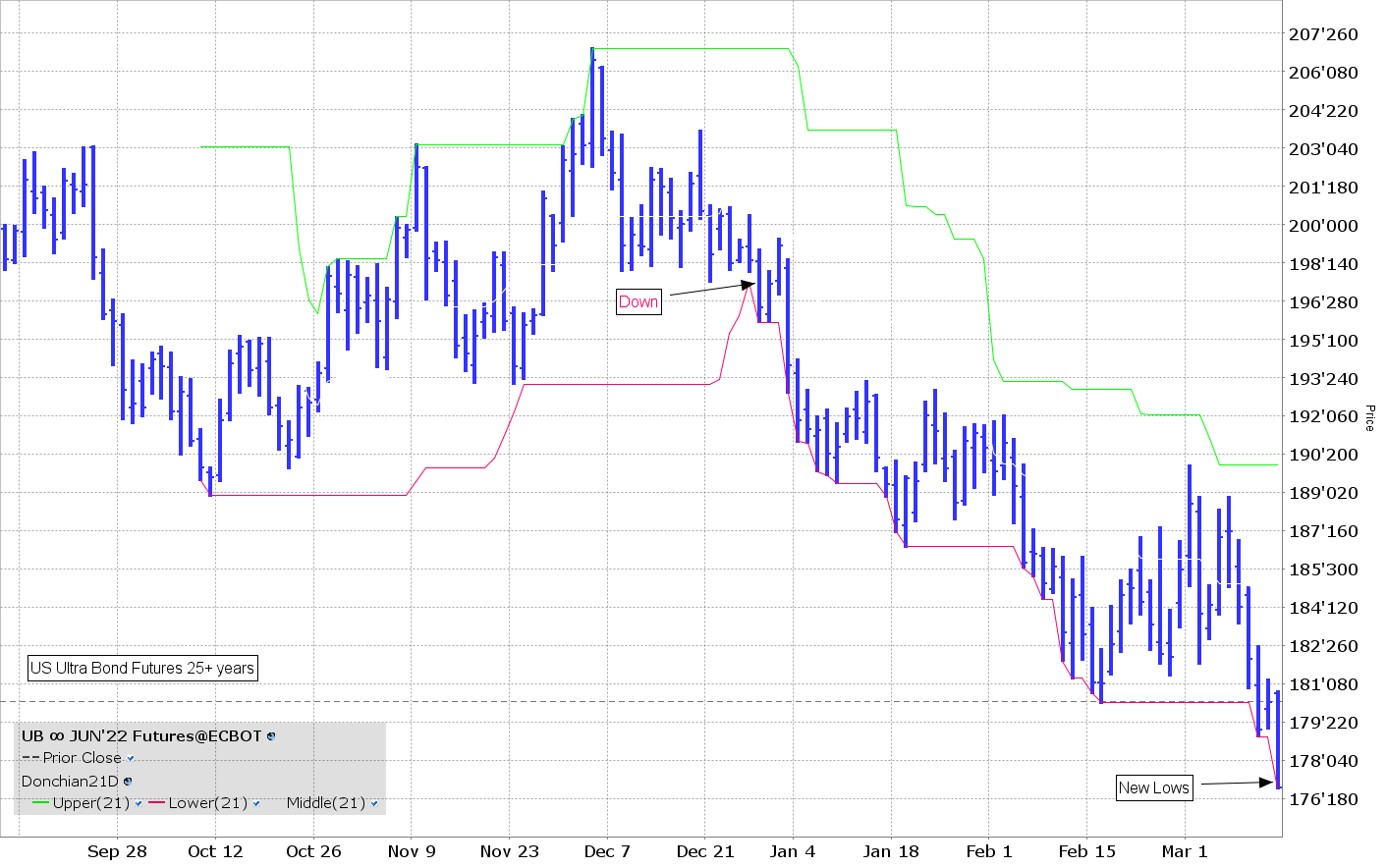

Below is a picture of the Ultra Bond (25+ year) futures contract. On Monday it was hitting new lows showing a 10% down move from the Donchian Channel 21 Day indicator sell signal I used on the chart for illustration purposes.

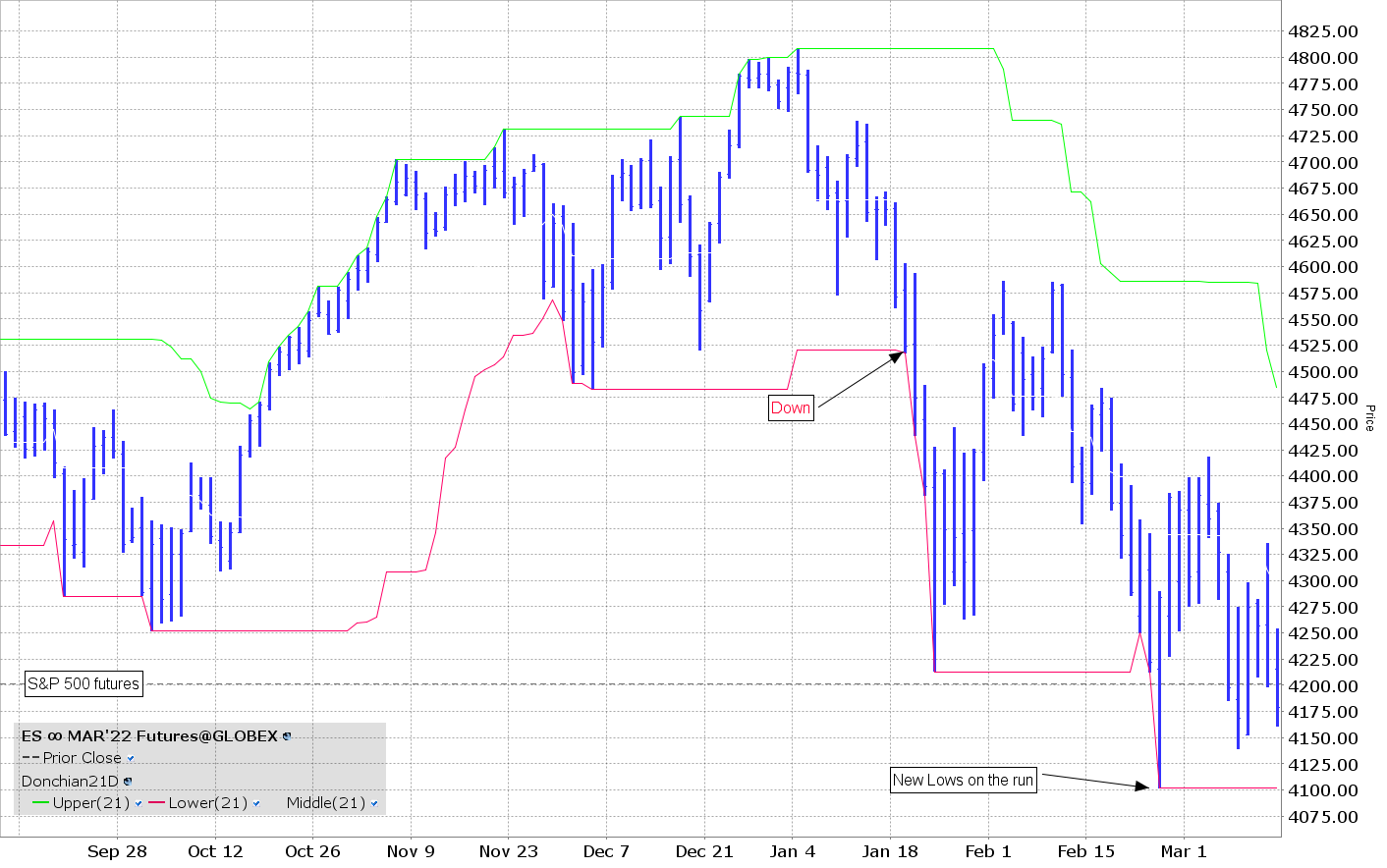

The other part of the 60/40 portfolio is 60% in stocks and they aren’t doing much better. Shown below is an image of the S&P500 Index futures contracts down -9.3% to the recent new lows on the run.

So you now have two parts of the portfolio comprising ALL of the portfolio that are sucking wind right now. Should retail investors be concerned?

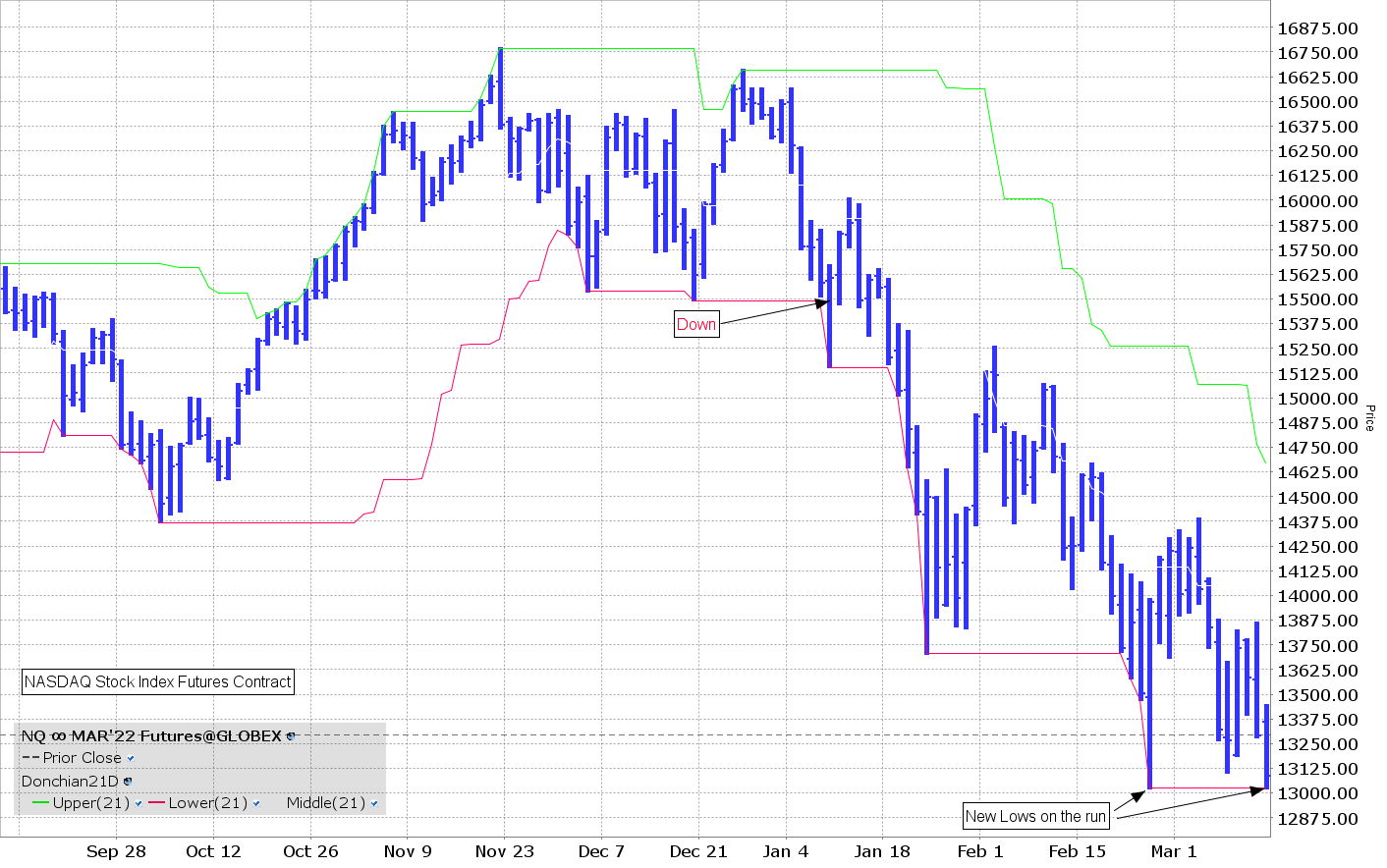

Moving over to the economy, right now you have real estate in some places so ridiculously high priced, buyers are getting priced out of the market. You have interest rates trending upwards. (see bond chart above) You have stocks in a down trend. The Nasdaq index is now down in bear market territory from highs (-20%) and -16% down from the direction shift to down in January.

Record energy and food prices are not going to help the economy thrive either. Lately, I have seen so many crazy moves in so many futures markets that I trade, I’ve almost become numb to the events. Wall Street houses are upping their probabilities of a recession in the next year. And, we have a war in Ukraine that doesn’t seem to be getting resolved yet.

Many would say the US economy has been recovering from COVID and is the strongest economy in the world and I would tend to agree with them. But how much weight can the US economy carry on its back before collapsing under the strain?

As many have heard me say over and over, I don’t predict when trading. The direction moves to up, I’m long. When it moves to a down direction, I’m out or short. “Keep it very simple” would be my motto in trading.

But, an investor creating and maintaining a 60/40 portfolio may see both sides of their portfolios struggling at the same time, testing their psyche in “buying and holding” down the road as the economy sputters, interest rates are increased to battle inflation and stocks see tougher conditions to continue increasing earnings. The way things look right now, this could go on for quite a while. Past swings down in both the bond and stock markets have seen -50% or more moves. Most long-term investors will not stick around for that, or will be devastated when they wake up to losing half their portfolio. I can hear them saying, “That wasn’t supposed to happen with my portfolio in a ‘conservative’ 60/40 strategy.”

This is essentially why I have spent so much time over the last decade diversifying into multiple strategies, multiple time periods and multiple macro markets outside of stocks and bonds. If being long stock/bonds are not the place to be, then put yourself somewhere else, where the wind is at your back, and enjoy the ride!

I keep thinking of this 2003 comment from Bruce Kovner, "The inflation, volatile exchange rates, rising commodity prices and high nominal interest rates that followed in the 1970’s created an environment in which the old ways of investing no longer functioned well. Long-only stock and bond trading were not the optimum ways to capture the opportunities that the 1970’s created. On the contrary, between 1968 and the early 1980’s, stocks and bonds suffered through a long bear market, destroying the value of equity and bond portfolios and undermining confidence in traditional investing styles. On the other hand, opportunities to profit from being long or short in currencies, fixed income, stocks and commodities abounded. The stage was set for active ‘macro trading’ as the increasingly popular term would label it." https://www.brucekovner.com/Caxton20thAnniversary.html

It sure does feel to me that we are returning to the 70's in that regard. Maybe only with more volatility and higher misery indexes.