Size Really Does Matter!

Size Really Does Matter!

A simple study of position sizing

A recent interview request had me creating an Excel spreadsheet on a simple timing strategy using SPY data that I had already downloaded from Yahoo Finance. The goal was to show the positive effects on return to risk and the trader’s peace of mind.

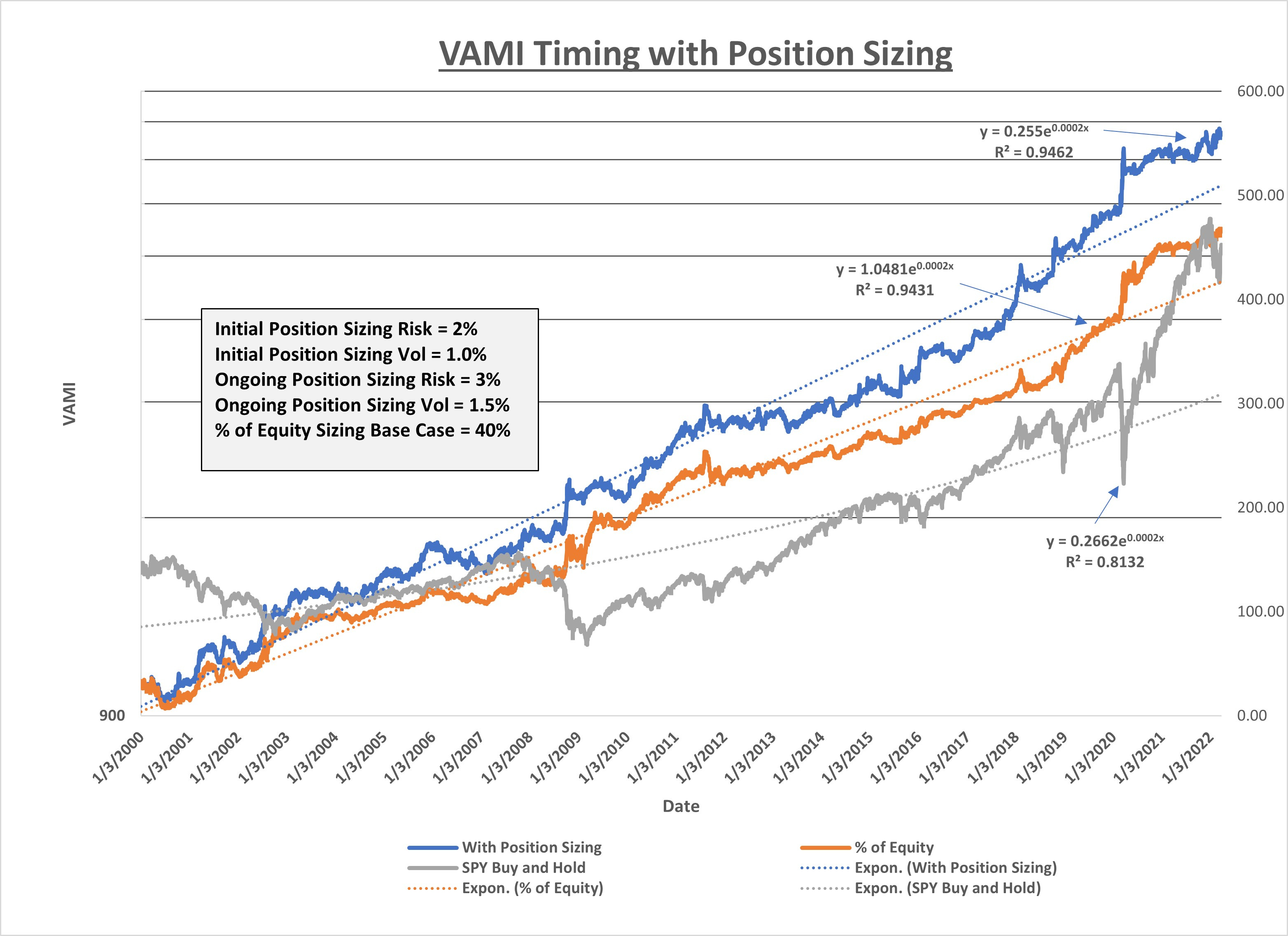

The data covered a lengthy period from January 2000 all the way to last Friday, the 25th of March, 2022. I preset some fairly normal risk and volatility levels in the SPY position that most traders might find comfortable. Initial risk as a percent of equity was 2% of equity. Initial position size due to volatility as a percent of equity was set at 1%. Ongoing risk and volatility percentages of equity were set at 3% and 1.5% respectively. This concept and all the formulas are laid out in my book: Successful Traders Size Their Positions - Why and How? if you want more details.

What I found wasn’t much of a surprise to me, since I’ve been using risk and volatility measurements to set my positions sizes for decades now. No matter how many studies I do, I always seem to find that managing your position size throughout the trade helps smooth out the equity curve and improves the return to risk, allowing me to sleep better at night.

The blue line uses position sizing limits to select the number of shares traded on each trade. The orange line sets it position size using a % of the dollars in the portfolio which I set at 40% in this study. Finally the gray line is simply the closing price each day of the SPY SPYDR etf.

The first and most obvious thing I notice is the wild ride you take if you buy and hold the etf. I personally could not stand the wild ups and downs and much prefer to attack that risk using timing to mitigate risk.

Second, the R-squared of the risk and volatility sized positions is very slightly better than the percent of assets case, a more traditional way of looking at sizing a position. And for fairly tame sizing parameters shown above, the trader ended up with a little more profit at the end of the simulation.

If you are interested maxing out your profits, feel free to “go for it”. As for me, I’ll logically size my various positions and enjoy the ride!

Hi Tom

I found your book on position sizing to be a gem and critical to my success and stress reduction :) to make sure I am following position sizing correctly, if you may I wanted to clarify with you. 1) When you say better risk to reward outcome can be attained by combining both equity risk allocation and volatility risk (say 0.5% each) when determining position size ...do you mean we give 50% weightage to outcome of each position zing algo in other words taking average of both methods to calculate a position size ? and not go for lower of the two. 2) When you say the total portfolio should be kept at 12.5% do you mean for a given day any move could result in maximum loss of 12.5% if all say 8 or 12 or 20 or more position go against one and move 1 to 2 ATR on a given day ?

Looking forward to your clarification, many thanks for writing such as excellent book on position sizing it has made it simple, easier and effective to adopt position sizing in one trading.

Great article. Quick question. What entry/exit rule that the simulation use regarding the blue line? Thank you